Klarna's IPO: A Blueprint for BNPL Success and Lessons for Latin American Players

The buy now, pay later (BNPL) industry has reached a critical inflection point with Swedish fintech giant Klarna's filing for an IPO on the New York Stock Exchange under the ticker symbol "KLAR." As a 19-year-old pioneer in the space, Klarna's journey from a small Swedish startup to a global financial powerhouse offers valuable insights for emerging BNPL players in Latin America, where companies like Pagaleve (Brazil), Kueski (Mexico), and Addi (Colombia) are following similar trajectories, albeit at earlier stages.

Klarna's Path to IPO: Business Overview

The company's journey began with a simple yet powerful idea: bridging uncertainty in online transactions by allowing consumers to pay after receiving goods. At a time when e-commerce was still nascent and marked by consumer distrust, this innovation addressed a critical market need. By 2010, they had expanded their offerings to include Pay in Full, and by 2017, they began building a disruptive brand focused on helping consumers streamline their financial lives. The acquisition of a banking license that same year proved to be a transformative milestone in their evolution.

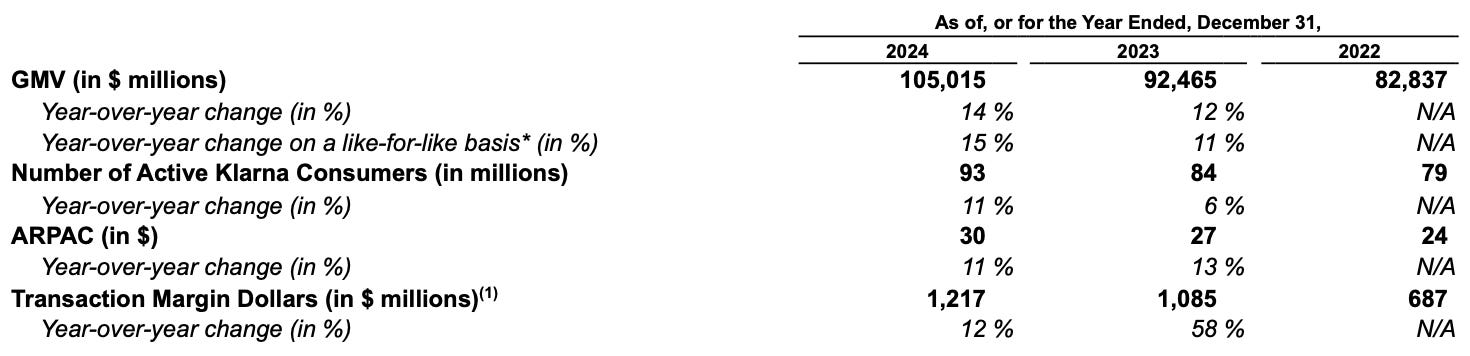

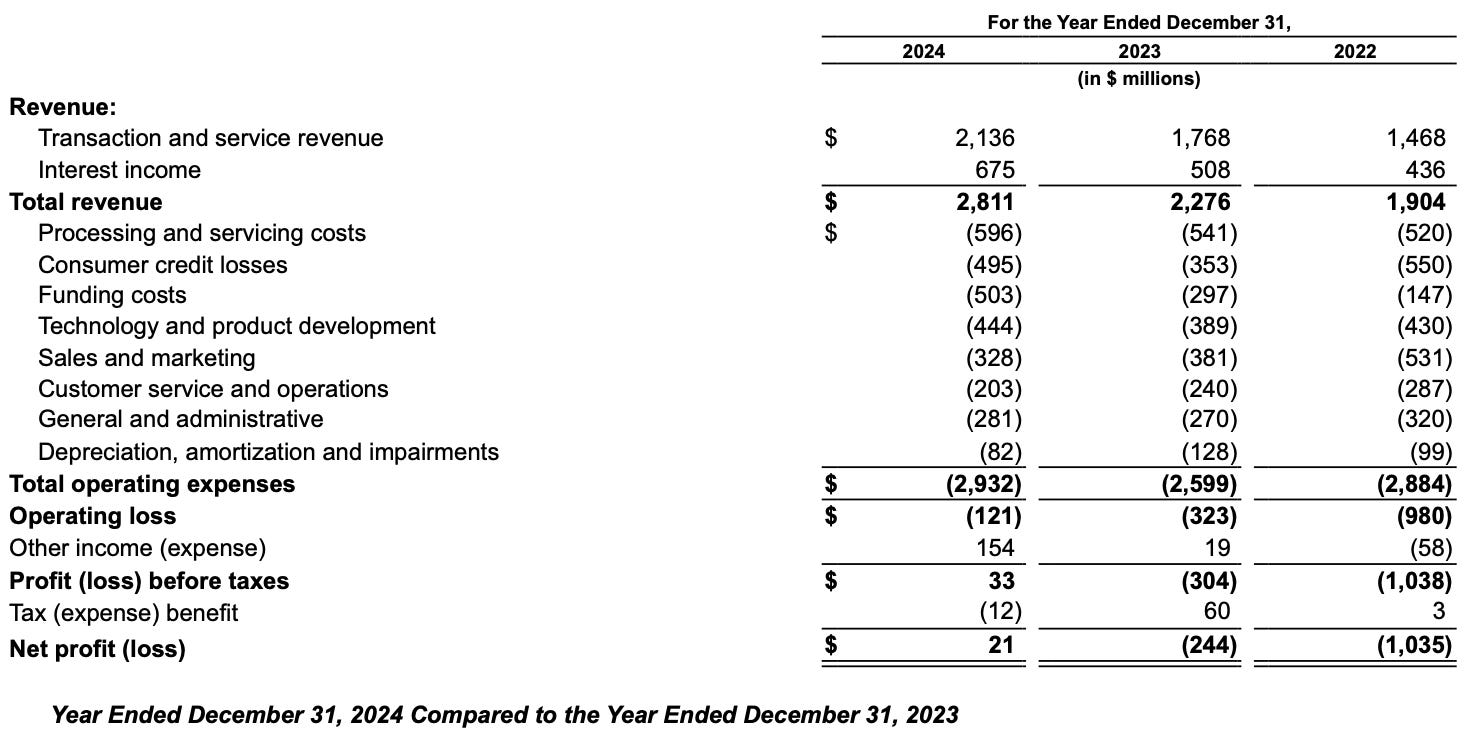

According to their F-1 filing, Klarna has built "one of the largest commerce networks in the world," serving approximately 93 million active consumers and more than 675,000 merchants across 26 countries as of December 2024. The company facilitated an impressive $105 billion in Gross Merchandise Volume (GMV) in 2024 alone. What's particularly notable is how they've achieved this scale while maintaining strong financial performance - in 2024, their total revenue reached $2.8 billion, representing 24% year-over-year growth, while their operating loss improved by 63% to $121 million.

This consumer growth has been remarkable, with active Klarna consumers increasing from 79 million in 2022 to 93 million by the end of 2024 - an 18% increase in just two years. This growth demonstrates Klarna's ability to continuously expand its consumer base even in mature markets, positioning the company as an increasingly essential partner for merchants looking to reach digitally-savvy shoppers.

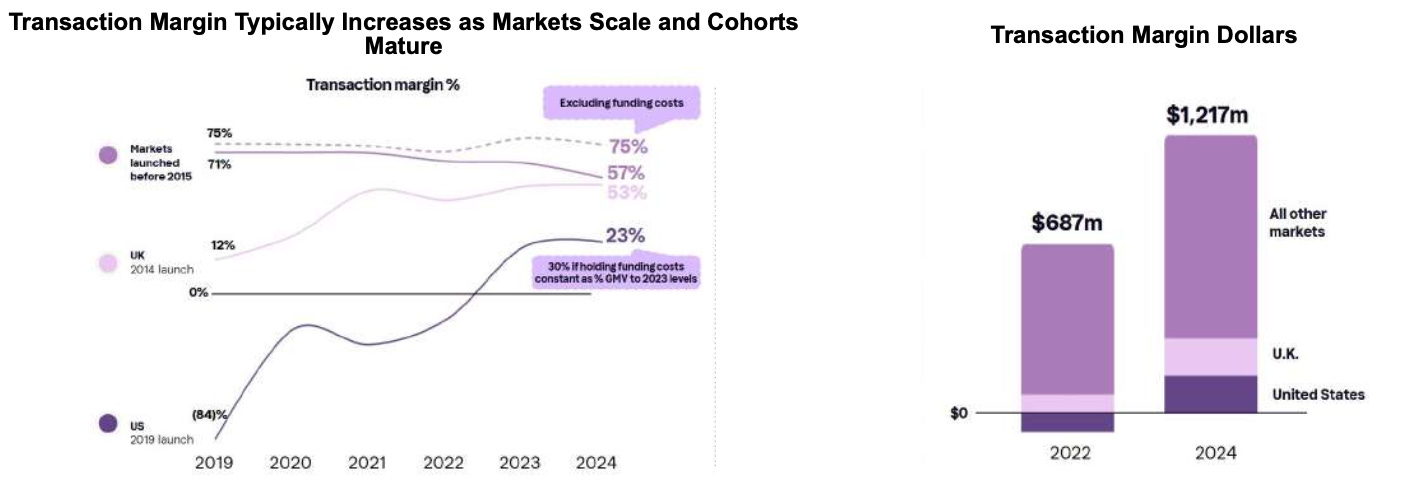

The company's transaction margin – perhaps the most critical metric for assessing BNPL sustainability – has shown consistent improvement. Transaction margin dollars equaled $1.2 billion in 2024, representing 12% year-over-year growth. This trend demonstrates Klarna's ability to monetize its network while managing risk effectively. Their transaction margin has expanded from 36% in 2022 to 43% in 2024, showcasing the power of their operational leverage as they scale.

What's particularly instructive is how transaction margins evolve as markets mature. Data from Klarna's F-1 shows that markets launched before 2015 (including Sweden, Norway, Finland, Germany, Netherlands, Austria and Switzerland) currently generate transaction margins of approximately 57%, while the UK (launched in 2014) achieves 23%, and the US (launched in 2019) has improved from negative 84% at launch to 23% in 2024. This pattern of margin improvement as markets mature provides a roadmap for Latin American players contemplating their own growth trajectories.

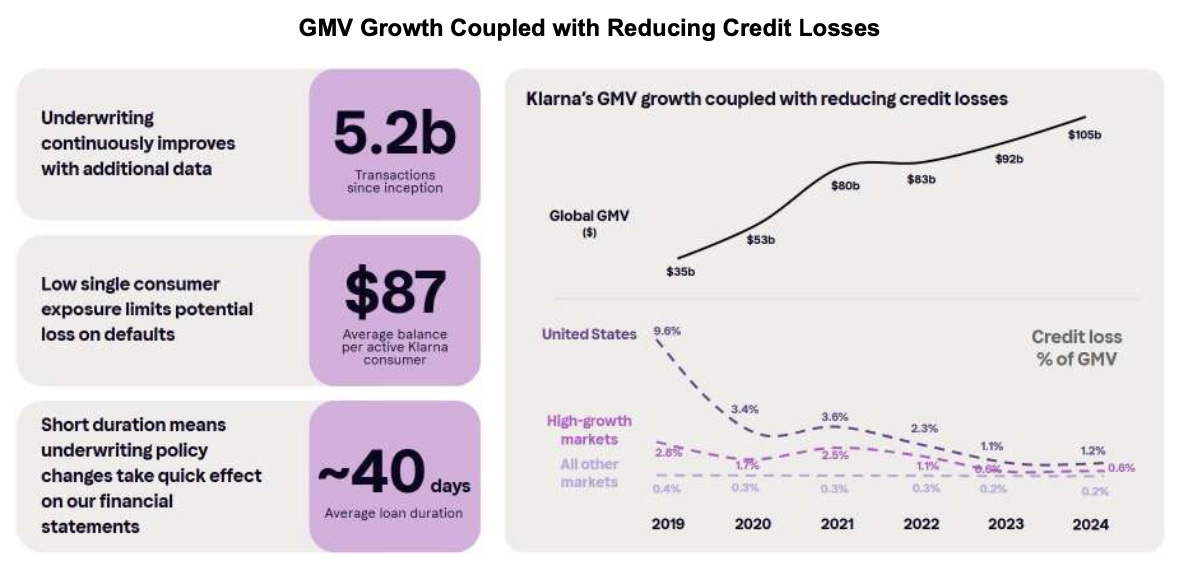

Credit performance metrics reveal a sophisticated risk management approach. In 2024, Klarna's consumer credit losses represented just 0.47% of GMV, significantly outperforming industry averages. For comparison, the F-1 notes that "loan losses as a share of total loans averaged 3.7% for [Klarna's] main competitors in Sweden in 2023." This superior performance stems from their unique underwriting capabilities, which leverage proprietary data from approximately 2.9 million daily transactions across their network.

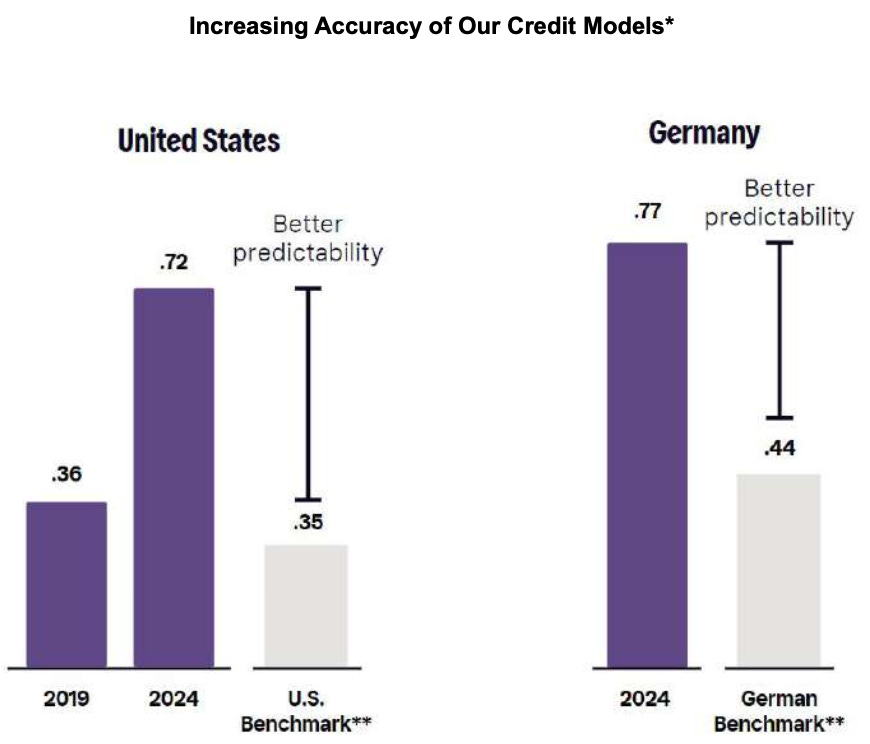

The company's credit underwriting model has improved dramatically in a short period. In the United States, Klarna has increased its Gini score (a measure of predictive accuracy in credit models) from 0.36 in 2019 to 0.72 in 2024 - exceeding the US benchmark score of 0.35. This improvement reflects the power of Klarna's machine learning models and data advantage, which have allowed them to reduce credit losses in the US from 9.6% in 2019 to just 1.1% in 2024.

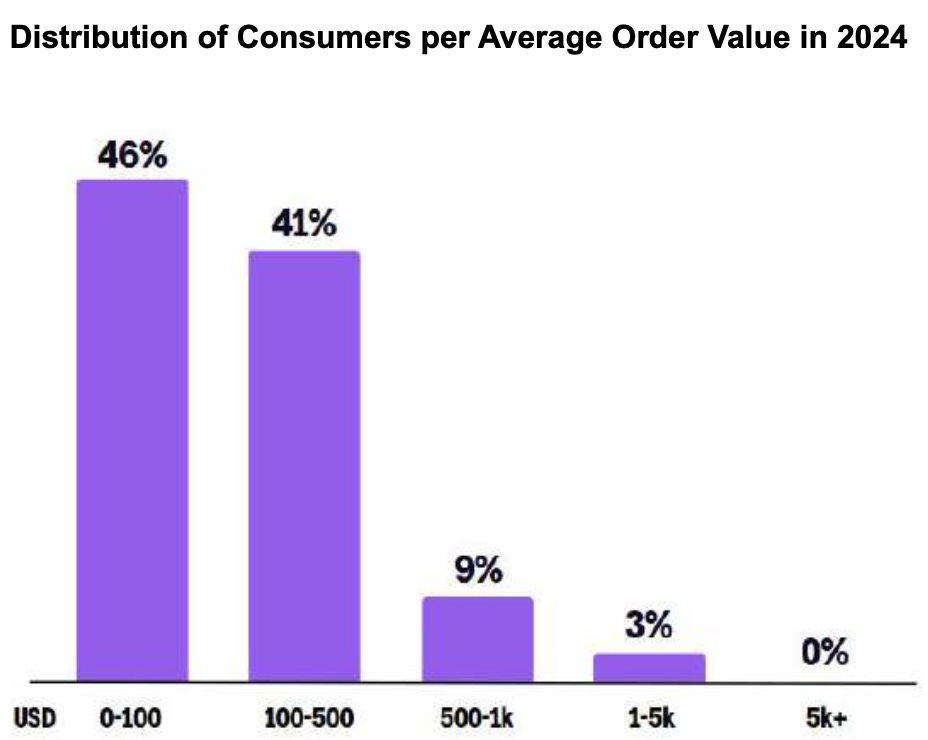

A key factor in this exceptional credit performance is Klarna's focus on small-ticket, short-duration transactions. Their average balance per active consumer was just $87 in 2024, with an average loan duration of approximately 40 days. As the distribution data shows, 87% of their orders in 2024 were $500 or less, with 46% under $100 and 41% between $100-500. This concentration on smaller transactions limits potential losses upon default and allows for rapid portfolio adjustment when economic conditions change.

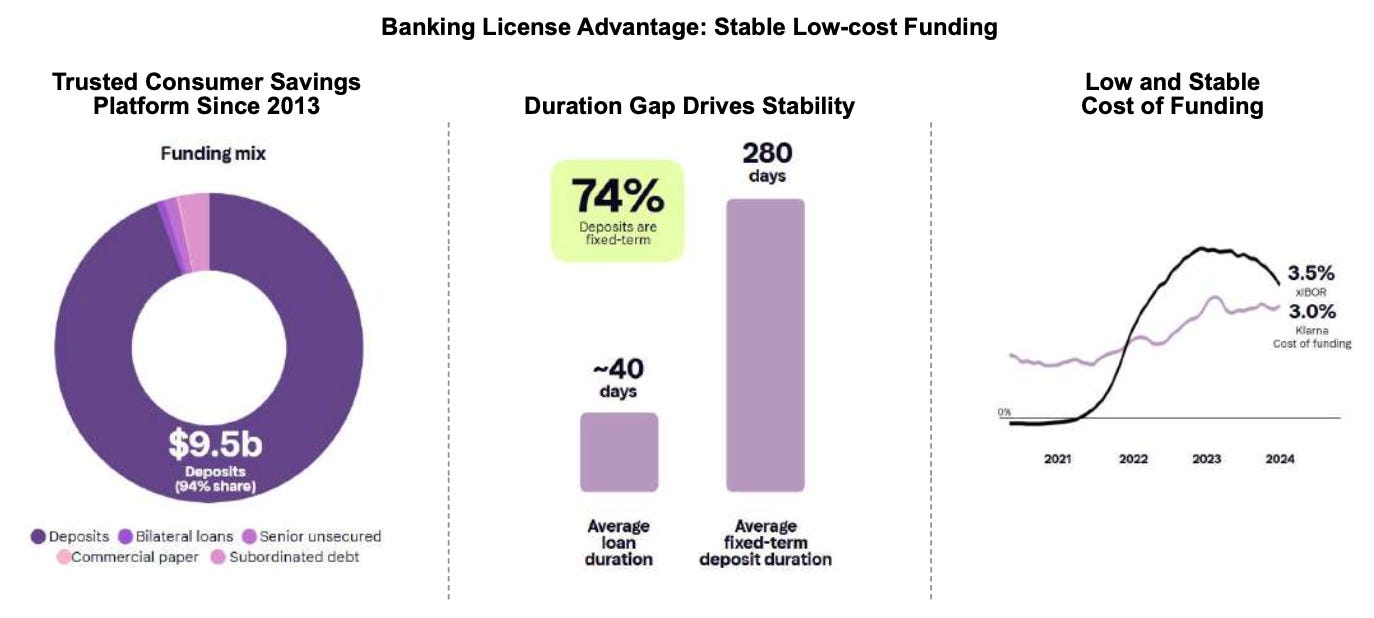

The funding model provides a significant competitive advantage. As of December 2024, Klarna held $9.5 billion in consumer deposits, which funded 94% of their financing products. This deposit-based approach offers substantially lower costs compared to wholesale or asset-backed financing arrangements that many non-bank competitors must rely on. Klarna's funding costs averaged 2.9% in 2024, compared to xIBOR rates in Europe of approximately 4.2% - a difference that translates directly to improved margins.

The inherent duration gap between Klarna's 40-day average loan duration and their 280-day average fixed-term deposit duration (with 74% of deposits being fixed-term) provides significant stability to their funding model. This mismatch allows Klarna to maintain low and predictable funding costs even in volatile interest rate environments, while also enabling them to rapidly adjust their loan portfolio if economic conditions deteriorate.

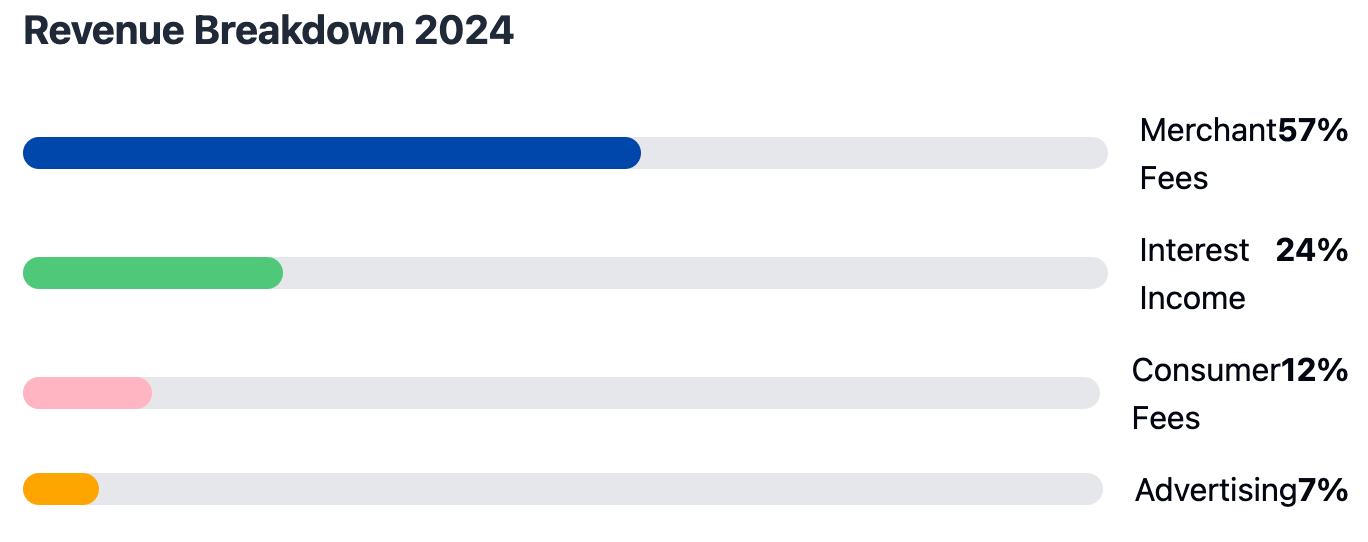

Revenue diversification has been another key strength. While payment processing fees from merchants remain their primary revenue source, Klarna has successfully expanded into advertising, generating $180 million in 2024 (up from approximately $13 million in 2020). This demonstrates their evolution beyond pure payments into a comprehensive commerce platform – a transformation that Latin American players would be wise to study.

Klarna's payment mix has evolved strategically over time. In 2022, Pay in Full represented 26% of GMV, Pay Later 70%, and Fair Financing 4%. By 2024, this mix had shifted to 16% Pay in Full, 79% Pay Later, and 5% Fair Financing - reflecting a deliberate focus on their core Pay Later products, which generate optimal economics. This product mix evolution provides insights for Latin American players on how to optimize their own offerings for maximum revenue and profitability.

Merchant relationships have been a key driver of Klarna's growth, with the company establishing partnerships with leading global brands across diverse verticals. The impressive penetration of top merchants in various markets - from 64% of top 100 merchants in Sweden to 29% in the United States - demonstrates their success in becoming an essential commerce partner. These partnerships create a virtuous cycle, where merchant adoption drives consumer acquisition, which in turn attracts more merchants.

The data from Klarna's partnership with On (maker of high-performance running shoes) illustrates the powerful growth dynamics these relationships can create. From 2020 to 2024, On's share of checkout with Klarna grew from 12% to 32%, while GMV increased 5x and revenue 9x. This case study demonstrates how Klarna's value proposition becomes increasingly compelling to merchants over time as they experience the benefits of higher conversion, larger basket sizes, and increased consumer loyalty.

Perhaps most impressive is Klarna's success in penetrating the U.S. market, where they've grown from a near-standing start in 2019 to becoming a significant player. Their GMV in the U.S. has grown by $19 billion over this period, and importantly, they began generating positive Transaction margin dollars in the market in 2023. This international expansion playbook offers valuable lessons for Latin American BNPL providers contemplating cross-border growth.

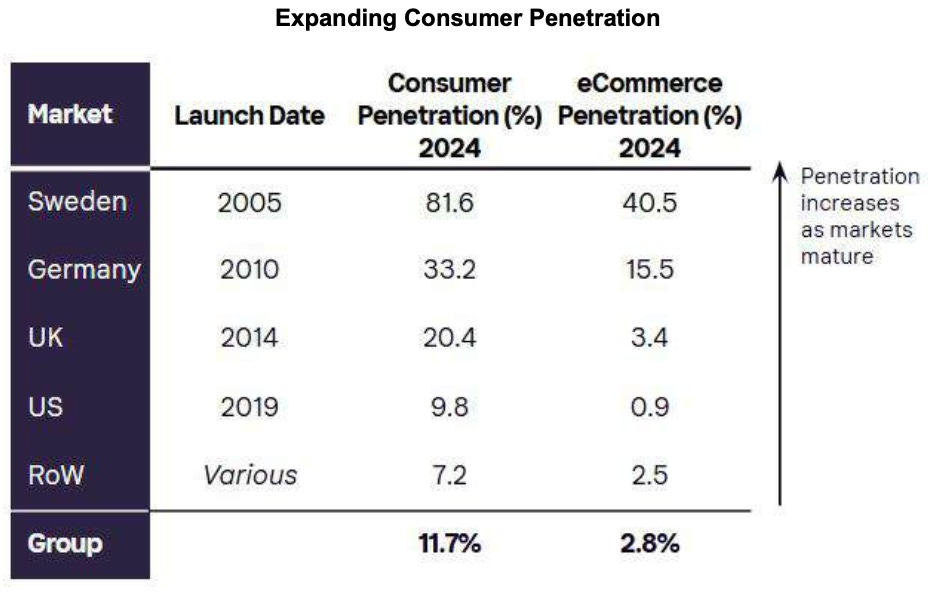

The expansion pattern revealed in Klarna's consumer penetration data provides insights into the BNPL adoption lifecycle. In Sweden, their most mature market (launched 2005), consumer penetration reached 81.6% by 2024. In comparison, Germany (launched 2010) achieved 33.2% penetration, the UK (launched 2014) reached 20.4%, and the US (launched 2019) attained 9.8%. This pattern suggests that sustained penetration growth continues for many years after market entry, providing confidence in the long-term growth potential for Latin American BNPL players who are earlier in their market development.

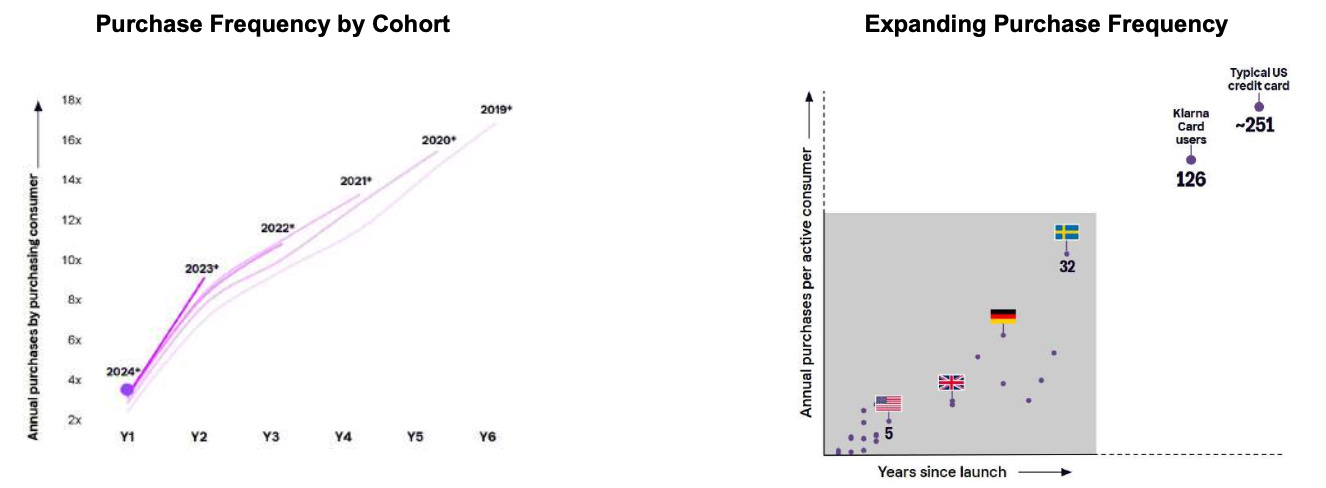

The increasing purchase frequency among Klarna's customers further demonstrates the network's growing utility. Average purchase frequency increased from 10.4 times per year in 2022 to 11.3 times in 2024, with significant variation by market maturity. In Sweden, their most mature market, consumers transacted 32 times annually by 2024, compared to just 5.4 times in the newer US market. This progression illustrates how consumer engagement deepens over time as markets mature and familiarity with BNPL increases.

Looking at cohort data, Klarna's consumer base demonstrates impressive purchase frequency growth over time. The 2019 consumer cohort made approximately 4 purchases in their first year but reached nearly 16 purchases by year six. Similarly, the 2020 cohort reached 15 purchases by year five. This cohort behavior shows how Klarna cultivates increasing loyalty and engagement over a consumer's lifecycle - a pattern that Latin American players should seek to replicate.

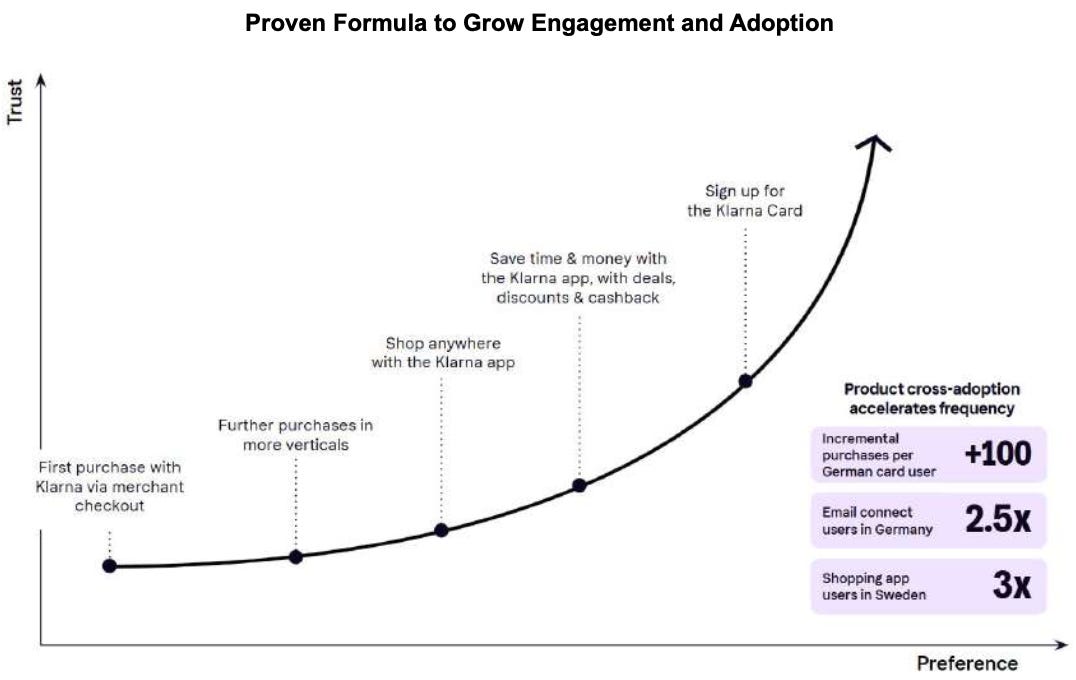

Klarna's proven formula for growing engagement and adoption follows a clear progression curve: from first purchase via merchant checkout, to additional purchases across verticals, to shopping anywhere with the Klarna app, to using Klarna for deals and cashback, and finally to signing up for the Klarna card. This increasing engagement drives trust and preference, with each new product adoption accelerating purchase frequency. For example, German card users made 100 more purchases per year compared to non-card users, and email connect users transacted 2.5 times as frequently as non-email connect users.

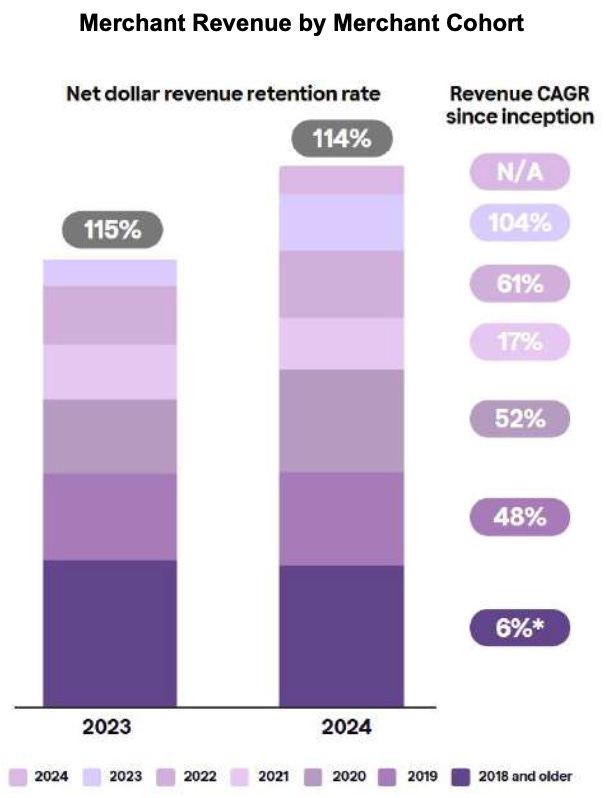

The company's revenue model has proven remarkably resilient, with strong merchant revenue retention. Klarna achieved net dollar revenue retention rates of 115% in 2023 and 114% in 2024, demonstrating their ability to expand revenue from existing merchants. Merchant cohorts from as far back as 2018 continue to grow revenue at impressive rates, with the 2023 cohort achieving a 104% CAGR since inception. This retention and expansion success illustrates how Klarna creates lasting value for merchants, rather than merely serving as a transactional payment option.

These financial results position Klarna favorably for its upcoming IPO, with the company achieving profitability in 2024 ($21 million net profit) after several years of strategic investment in growth. The path to profitability has been powered by Transaction margin expansion, disciplined operating expense management, and increasing operational leverage. From 2022 to 2024, Klarna's operating loss improved by an impressive $859 million, transforming from a $980 million loss to a much smaller $121 million loss - a testament to the scalability of their business model.

Klarna's Competitive Advantages and Strategic Assets

Several key factors have positioned Klarna for IPO success, providing a blueprint for Latin American BNPL players:

1. Banking License and Deposit-Based Funding

First and foremost is their banking license and deposit-based funding model. As stated in their F-1:

"We have operated as a licensed bank in the EEA since 2017, when the SFSA approved our application for a bank license. This license reinforced our position as a stable, trustworthy institution among our consumers and merchants."

This regulatory status enables Klarna to fund 94% of its financing products through deposits ($9.5 billion as of December 2024), providing a lower-cost and more stable funding base than non-bank competitors. This creates a virtuous cycle where deposits fund loans, which generate revenue, which attracts more deposits.

The funding advantage is clearly illustrated in Klarna's financials, where their average cost of funding was approximately 2.9% in 2024, compared to xIBOR rates in Europe of approximately 4.2%. This differential provides Klarna with a structural margin advantage over competitors relying on wholesale funding or more expensive capital market solutions. Additionally, the duration gap between their 40-day average loan duration and 280-day average fixed-term deposit duration provides significant stability even during interest rate volatility.

The banking license also grants Klarna significant flexibility in product development. As their F-1 notes,

"Our banking license allows us to design and offer financial products and services that otherwise could require third-party partnerships."

This product development agility has been crucial to their ability to adapt to changing market conditions and consumer preferences.

2. AI-Driven Efficiency and Scale

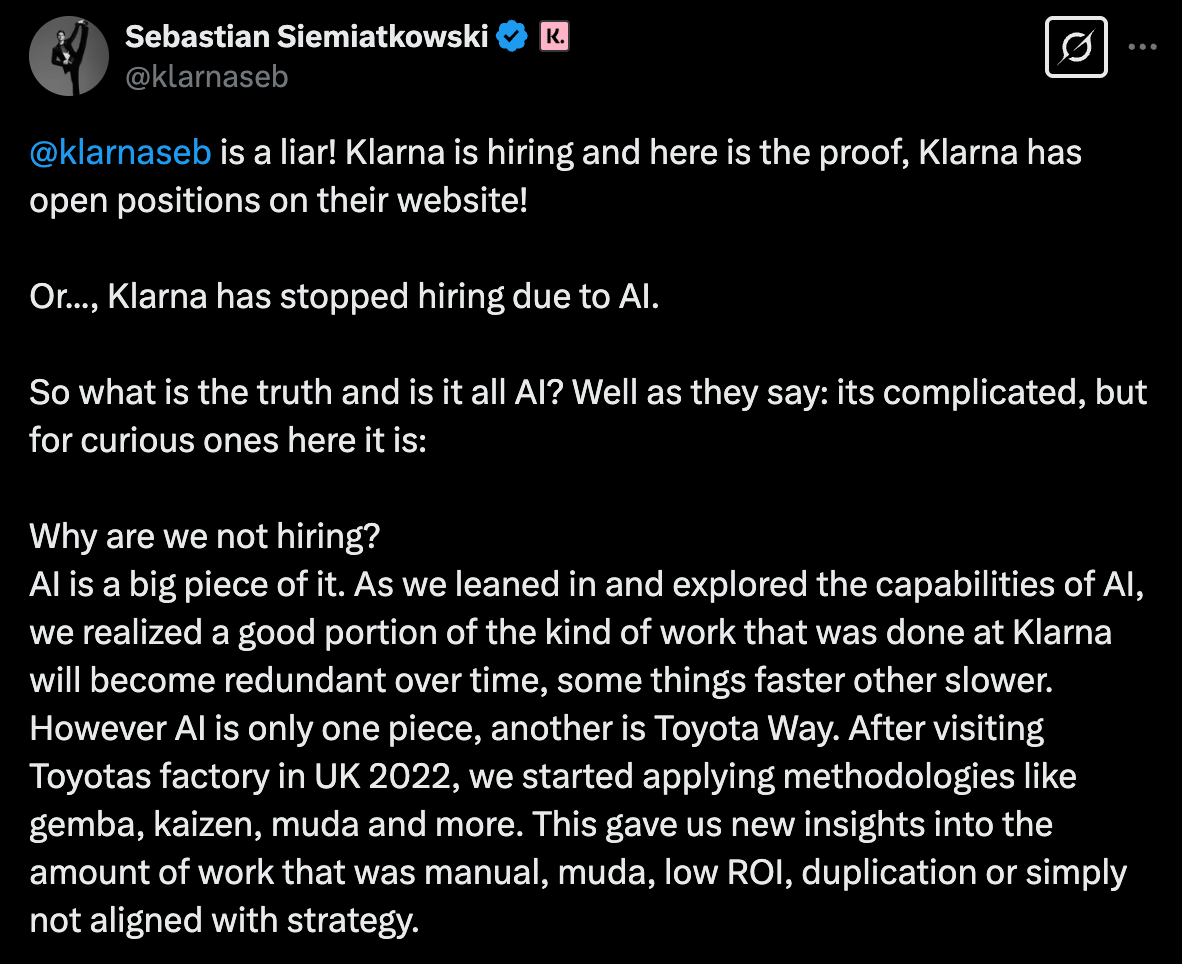

Second, Klarna has leveraged AI to drive remarkable operational efficiency. According to CEO Sebastian Siemiatkowski's statements about the company's hiring freeze,

"AI is a big piece of it. As we leaned in and explored the capabilities of AI, we realized a good portion of the kind of work that was done at Klarna will become redundant over time."

The results have been dramatic: their AI assistant has handled 62% of customer service chats since its launch, while maintaining the same customer satisfaction levels as human agents. More impressively, the company's average annual revenue per employee has increased from approximately $344,000 in 2022 to $821,000 in 2024 – a testament to AI-driven efficiency that far outpaces most financial services organizations.

3. Global Network Effects and Merchant Relationships

Third, Klarna has built powerful network effects across its ecosystem. As noted in their F-1:

"Our personalized, highly engaging consumer experiences drive consumers to our network. As more consumers engage at scale, more merchants join our network and grow their businesses. As more merchants join the network, consumers benefit from increased selection across verticals, channels and geographies."

These compounding network effects create a significant moat around their business.

The merchant success stories highlighted in the F-1 provide evidence of this network effect in action. With H&M, Klarna's share of checkout has reached nearly 50% across all markets, and in Sweden, 60% of orders from new customers are made through Klarna. Sephora has seen Klarna users shop 6.8 times per year on average, compared to 4 times for all Sephora consumers. Foodora experienced a 14% increase in Klarna consumer purchase frequency after using Klarna's advertising solutions. These examples demonstrate how Klarna creates value throughout the commerce ecosystem.

Strategic partnerships have further strengthened Klarna's position. A prime example is their recent deal with Walmart, which CNBC reported as "taking a coveted partnership away from rival Affirm." This arrangement includes warrants for OnePay (Walmart's fintech) to purchase Klarna shares, aligning the interests of both companies. As the F-1 notes, Klarna also partners with "several of the world's largest PSPs, including Worldpay, Stripe and Adyen" to enable seamless merchant onboarding.

4. Diversified Revenue Streams

Klarna has successfully diversified beyond pure BNPL fees. The company generated $180 million in advertising revenue in 2024, up from approximately $13 million in 2020. This diversification reduces dependence on transaction fees and creates additional value for both consumers and merchants.

According to the F-1: "Digital advertising represents an additional approximately $475 billion market opportunity globally (excluding China) in 2023 that we believe we are uniquely positioned to address given our unique data from intent-driven consumers."

5. Credit Underwriting and Operating Leverage

The company's proprietary data and sophisticated credit underwriting represent another significant advantage. Unlike traditional credit card issuers who typically make a single underwriting decision at account opening, Klarna makes real-time decisions for every transaction. Their credit model leverages machine learning and a unique dataset including "more than 2.5 billion SKU-level data points collected in 2024." This approach results in superior risk management, with consumer credit losses well below industry averages.

The improvement in Klarna's credit models is particularly evident in newer markets like the United States, where their Gini score (a measure of predictive power) improved from 0.36 in 2019 to 0.72 in 2024, far exceeding the U.S. benchmark of 0.35. This improvement allowed them to reduce credit losses in the U.S. from 9.6% in 2019 to just 1.1% in 2024 - a transformation that enabled positive Transaction margin dollars in that market.

Finally, Klarna's global scale provides significant operating leverage. Operating in 26 countries creates natural portfolio diversification while enabling the company to spread fixed costs across a larger transaction base. Their international presence also provides valuable diversification against local economic downturns – a consideration particularly relevant for Latin American players given the region's macroeconomic volatility.

Latin American BNPL Landscape: Current State and Growth Trajectories

The Latin American BNPL market, while still emerging compared to more mature regions, is developing rapidly with key players establishing strong positions in their respective markets. Each is navigating unique regional challenges while building scale and partnerships reminiscent of Klarna's early growth phase.

Kueski

In Mexico, Kueski has emerged as the leading BNPL provider, achieving remarkable milestones that demonstrate its growth trajectory. In October 2024, Kueski announced it had reached 20 million loans disbursed, representing 100% growth in just 18 months. The company now issues an average of one loan every two seconds, powered by innovative AI and machine learning credit decisioning models similar to those that have driven Klarna's success.

A significant recent win for Kueski was securing a partnership with Amazon Mexico in January 2024, becoming the e-commerce giant's first BNPL provider in the country. This achievement parallels Klarna's strategic focus on merchant partnerships, which has been central to their network growth. Kueski has also expanded its merchant network to include global brands like Estée Lauder, MAC, and Clinique, now boasting the highest penetration rate (nearly 30%) among the top 150 e-commerce merchants in Mexico.

Addressing Mexico's predominantly cash-based economy, Kueski launched an offline payment solution for physical stores that functions without internet connection – a crucial innovation in a country where, according to Banxico's 2023 study, 80% of transactions are still conducted in cash. This offline expansion strategy echoes Klarna's own move into physical retail through their Klarna Card and in-store payment solutions.

Addi

In Colombia, Addi has been making significant strides, with several notable developments that position it as that market's BNPL leader. In November 2024, Addi secured a $100 million credit facility from Victory Park Capital, following an $86 million equity and debt round earlier in March. This brings the company's total funding to $562 million since its founding in 2018 – impressive figures for a Latin American fintech and comparable to Klarna's early funding trajectory.

A key regulatory milestone for Addi was its successful acquisition of a banking license to operate as a regulated financial institution in Colombia. This strategic move closely resembles Klarna's own regulatory approach, positioning Addi to potentially develop a deposit-based funding model similar to what has proven so advantageous for Klarna in Europe.

Addi has also launched a marketplace platform, onboarding more than 500 merchants and processing over 20,000 monthly transactions within six months of launch. The company now serves approximately 2 million customers and 18,000+ merchants across Colombia. Perhaps most impressive has been Addi's ability to reach profitability in 2024 while maintaining a low 1% delinquency rate on loans – demonstrating strong underwriting capabilities in a market with limited credit data.

Pagaleve

In Brazil, Pagaleve has focused on leveraging the country's widely-adopted PIX instant payment system to offer installment payments, creating a uniquely Brazilian approach to BNPL. In February 2025, Pagaleve announced a strategic partnership with AliExpress to offer "PIX Parcelado" (installment payments via PIX) as a payment method. This allows Brazilian consumers to pay for purchases in up to 4 interest-free bi-weekly installments or 12 monthly installments with interest.

This integration with PIX is particularly significant given that the payment system is now used by 82% of Brazilians. By combining the immediate settlement benefits of PIX with installment capabilities, Pagaleve is creating a solution tailored to Brazilian market preferences. This localization strategy mirrors Klarna's own approach of adapting their products to local payment preferences and regulations.

Challenges & Market

While these Latin American players are making impressive progress, they still face unique regional challenges that Klarna did not encounter in its European expansion. Limited credit bureau data makes underwriting more challenging, while higher interest rate environments impact funding costs. Additionally, the predominantly cash-based nature of many Latin American economies requires innovative solutions to bridge the digital divide.

Nevertheless, the region presents compelling opportunities for BNPL. E-commerce penetration is growing rapidly, large unbanked populations remain underserved by traditional financial institutions, and credit card penetration remains low in many markets. These factors create natural demand for flexible digital payment solutions.

The Path Forward: What Latin American Players Can Learn from Klarna's Journey

Based on Klarna's journey to IPO, BNPL companies in Latin America should focus on several key strategic priorities:

1. Achieve Sustainable Unit Economics

First, achieving sustainable unit economics is paramount. Klarna's path to profitability is instructive. As noted in their F-1: "From 2022 to 2024, our Transaction margin dollars grew 77% to $1,217 million from $687 million." This improvement came from fee-driven revenue growth, scale efficiencies, declining credit losses, and improved operational leverage. Latin American players must similarly focus on transaction-level profitability before pursuing aggressive growth.

Addi's achievement of profitability while maintaining low delinquency rates demonstrates that sustainable economics are possible in the region despite macroeconomic challenges. Kueski's rapid scaling to 20 million loans suggests it too is finding viable unit economics in Mexico. Latin American players should closely monitor their transaction margins and be willing to slow growth in segments or verticals where margins are unsustainable.

2. Secure Strategic Funding and Partnerships

Second, securing strategic funding and regulatory advantages is critical. Klarna's banking license and deposit base provide significant competitive advantages that have been central to their success. As their F-1 notes, "Our banking license enables us to maintain a low-cost, stable funding model based on consumer deposits." This funding advantage has been crucial to Klarna's ability to offer competitive merchant fees while maintaining profitability.

Latin American players are pursuing different approaches based on their market circumstances. Addi's acquisition of a banking license in Colombia represents a major step toward replicating Klarna's model. For players without banking licenses, strategic partnerships with established financial institutions may provide an alternative path to stable, cost-effective funding.

3. Invest in Proprietary Technology and AI

Third, investing in proprietary technology and artificial intelligence capabilities will be essential. Klarna's technological prowess, particularly in AI, has been crucial to its efficiency and risk management. According to their F-1: "As of August 31, 2024, 96% of our employees used generative AI in their daily work." This widespread AI adoption has enabled Klarna to significantly increase revenue per employee while improving customer experiences.

The Latin American players are similarly embracing technology. Kueski highlights its "innovative AI and machine learning-powered credit decisioning models," while Addi's low delinquency rates suggest sophisticated risk modeling. As these companies grow, continued investment in AI capabilities will be critical to achieving Klarna-like operating efficiencies and credit performance.

4. Expand Beyond Core BNPL

Fourth, expanding beyond core BNPL into adjacent services represents a significant opportunity. Klarna has successfully evolved from a payment method to a comprehensive commerce network. Their F-1 describes a vision where "Klarna empowers everyone, everywhere, through seamless commerce experiences—as a personalized, trusted assistant making financial empowerment effortless."

We're seeing early signs of similar expansions in Latin America. Kueski's offline payment solution shows understanding that commerce happens beyond e-commerce. Addi's marketplace launch demonstrates movement toward becoming a shopping destination rather than just a payment method. As these companies mature, further expansion into advertising, merchant services, and additional financial products will likely follow Klarna's diversification playbook.

5. Build A Trusted Brand for Merchants and Consumers

Fifth, building strong merchant relationships is crucial for sustainable growth. Klarna's merchant network includes "some of the largest global brands," with an average of "44% of the top 100 merchants in each of the major markets" they serve. These relationships provide both scale and credibility. Latin American players should prioritize strategic merchant partnerships, particularly with major regional e-commerce platforms and retail chains.

Finally, developing a recognizable and trusted consumer brand will be essential for long-term success. Klarna has built what they describe as "a brand that is distinctly global, universally recognized and well-loved by consumers and merchants." Their global NPS of 73 demonstrates exceptional consumer loyalty. Latin American BNPL providers should invest in building trusted brands that resonate with local consumers while maintaining the global appeal necessary for eventual international expansion.

Conclusion: The BNPL Opportunity in Latin America

Latin America represents a compelling opportunity for BNPL, with high e-commerce growth rates, significant unbanked populations, and limited credit card penetration. The region's BNPL leaders are making impressive progress, adapting global best practices while solving for local market needs.

Klarna's upcoming IPO provides a valuable roadmap for Latin American BNPL aspirants. The Swedish company's journey from payment processor to global commerce network demonstrates the potential evolution path for companies like Kueski, Addi, and Pagaleve. By focusing on sustainable unit economics, securing strategic funding, investing in technology, expanding beyond core offerings, and building trusted brands, these companies may well follow Klarna to the public markets in coming years.

The unique characteristics of Latin American markets will require continued innovation and adaptation. The prevalence of cash transactions, limited credit bureau data, and varying regulatory environments across countries create challenges distinct from those Klarna faced in Europe. However, these same factors create opportunities for companies that can effectively bridge the digital divide and provide financial inclusion.

As Klarna CEO Sebastian Siemiatkowski noted in their F-1 filing, "The future of AI and everything is we're going to have digital financial assistance agents that can go and negotiate on your behalf with banks." This vision of AI-powered financial services points to where the industry is heading globally, including in Latin America.

For investors and industry participants watching the Latin American BNPL space, the rapid progress of companies like Kueski, Addi, and Pagaleve suggests that the region may produce its own Klarna-sized success stories in the coming years. While the path to IPO will undoubtedly include challenges, the foundation being laid today – built on both global fintech trends and the unique characteristics of Latin American commerce and consumer behavior – provides reason for optimism about the region's BNPL future.

As the global BNPL landscape continues to evolve, Latin American players have the advantage of learning from Klarna's two-decade journey. By applying these lessons to their unique regional context, they may not only replicate Klarna's success but potentially surpass it by creating innovative models tailored to the specific needs of Latin American consumers and merchants.

Great read!

Top article!